Palladium Market: Major Facts and Statistics to Know in 2018

04 Sep 2018 • by Natalie Aster

LONDON – Palladium is a rare silvery-white metal that falls into the platinum group metals category. It was introduced by William Hyde Wollaston in the year 1803. Owing to the unique characteristics as excellent catalytic properties, and high durability and corrosion resistance make palladium useful in a broad range of applications.

KEY END-USE APPLICATIONS

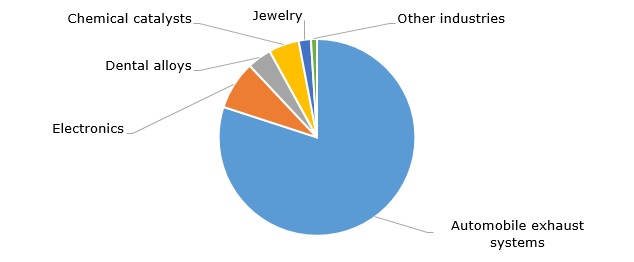

Nowadays, the automotive industry is the largest consumer of palladium: the metal is used in catalytic converters for exhaust systems, which convert almost 90% of the harmful gases in automotive exhaust into less hazardous substances. This end-use application captures a share of around 80% of the overall palladium consumption. The global automotive industry doesn’t show any signs of slowing down in the near future, and that is slated to ensure strong demand for palladium.

Palladium has also found applications across an array of other areas including electronics, medical, jewelry, groundwater treatment, hydrogen purification, various chemical sectors, amid others.

Structure of the palladium consumption broken down by industry, 2017

MINE PRODUCTION

The volume of the world’s palladium mine production demonstrated remarkable fluctuations during the past decade with the highest figure registered in 2007 and the lowest – in 2014. In the year 2015, it was slightly over 6.71 million ounces. In 2016, the world’s mine production of palladium witnessed a slight YoY decrease and totaled about 6.54 million ounces. In 2017, it recovered and exceeded 6.74 million ounces.

World’s palladium mine production over 2004 – 2017 (in million ounces)

.jpg)

Worldwide, ore deposits of all platinum group metals including palladium are rare. The vastest deposits of palladium have been found in Russia (the Norilsk Complex), South Africa (the Bushveld Igneous Complex), Canada (the Sudbury Basin and the Thunder Bay District), and the US (the Stillwater Complex in Montana). Therefore, these countries are the top palladium producers globally.

MAJOR PRODUCING COUNTRIES

Russia has been holding the top spot on the list of the world’s leading palladium producing countries during the past few years. The country’s output volume of palladium exhibited a sluggish YoY decline last year and totaled some 81 metric tons.

The runner-up is South Africa. The volume of the palladium mine production in South Africa jumped by 5 metric tons YoY in 2017 and climbed to 78 metric tons.

The third position in terms of the palladium mine production is held by Canada. The country’s output of palladium far legs behind the top two palladium producing countries. The volume of Canada’s palladium mine production witnessed a decline since 2015 and reached 19 metric tons in the past year.

Top palladium mine producing countries, 2012 – 2017 (in metric tons)

.jpg)

SUPPLY

Besides mine production, palladium is also recycled. Scrapped catalytic converters present one of the major sources of recycled palladium. Moreover, the rare minerals of cooperate and polarite also contain palladium. One more possible source of palladium extraction is to recover it from spent nuclear fuel or some other radioactive waste (as the nuclear fission reaction produces this element), but, this extraction method is not feasible.

The world’s overall supply volume of palladium has followed an upward trend since 2014 when it was appr. 8.08 million ounces. In 2017, the global palladium supply went over 8.94 million ounces.

World’s overall palladium supply over 2005 – 2017 (in million ounces)

.jpg)

TOP PRODUCING COMPANIES

As for the companies engaged in the palladium production, the Russian player, Norilsk Nickel, is the biggest palladium producer across the globe. Presently, Norilsk Nickel grabs a 39% share of the world’s total palladium output. In 2017, the Company reported a 6% YoY increase in its palladium production, which run to 2.78 million ounces.

The second position in terms of palladium production belongs to Anglo American Platinum Ltd. The Company posted total palladium production of about 1.035 million ounces in 2017.

Dominant palladium producing companies, 2017 (in thousand ounces)

.jpg)

CONSUMPTION

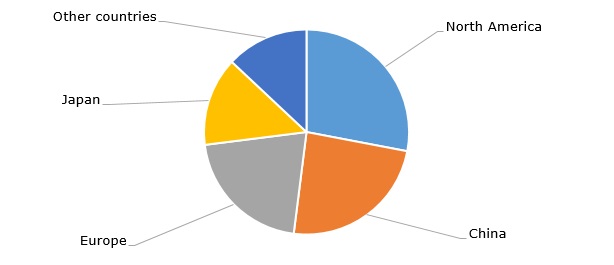

Geographically, North America is the major consumer of palladium accounting for a share of appr. 28% of the world’s total consumption volume. In 2016, the volume of palladium consumed by the North American region totaled more than 2.49 million ounces. It is followed by China and Europe grabbing shares of 24% (2.37 million ounces) and 21% (slightly above 2.35 million ounces), respectively

Structure of global palladium consumption by region, 2017

PRICES

2017 was a year of gains for the palladium: the price of this metal has gained considerably and amounted to USD 853 per troy ounce. In comparison, the price of troy ounce of palladium in 2016 was USD 614. Such a big hike in palladium prices is attributed majorly to the supply deficit coupled with the surging demand from the automotive sector.

Palladium average market price during 2009 – 2017 (in USD per troy ounce)

.jpg)

The mounting demand from a broad spectrum of applications along with the limited availability and supply result in high investment interest. Last year, the rate of return on palladium investments surged to nearly 56.2%. As of 2016, it was around 20.96%.

MARKET OUTLOOK

After a substantial growth in gross automobile catalyst demand as well as a remarkable upturn in palladium recycling in 2017, this year the world’s palladium market is poised to experience much smaller changes. Combined supply (mine production and recycling) is anticipated to go up by appr. 2%.

In the wake of the surging demand for palladium from the key end-use applications (especially the automotive industry) along with the dropping mine production volume, the palladium market shortfall is poised to surpass 1.2 million ounces this year. Meantime, in 2017 the palladium deficit was estimated at about 828 thousand ounces.

© MarketPublishers.com, 2018

Analytics & News