Key Trends Shaping Global Aviation Industry

28 Aug 2019 • by Natalie Aster

The worldwide aviation industry offers services to apparently any part of the globe and is also part and parcel of the world economy. It incorporates suppliers of air transport services for passengers and cargo alike. These services are used by individuals and organisations as well as governmental bodies from pole to pole.

Nowadays, the world aviation industry comprises above 2000 air companies that operate over 23,000 aircraft, rendering service to more than 3700 airports. The coming 20 years will require around 30,050 airplanes with their total value standing at over USD 5.6 trillion.

The aviation market is witnessing fast-paced growth worldwide and is projected to reach USD 832.8 billion in 2020 posting a 3.7% CAGR. Increased defense spending, largely from the developing nations, is likely to drive the procurement of combat aircraft, thereby boosting the aviation sector growth on the immediate horizon. Further, the urge for increased connectivity in today’s global economy, thriving tourism sectors, ongoing demand for new low-cost carriers (LCCs) and deregulation, growing disposable income of the middle-class in emerging markets have contributed a lot to an upsurge in the frequency of air travel and, thus, the aviation industry growth, especially in Asia and the Middle East. This has urged the aviation authorities and air carriers to take efforts with respect to investments in airport infrastructure, route expansions and provisioning of new aircraft deliveries resulting in additional seats. The replacement of old commercial airliners with brand new ones are also amid the key factors igniting the sector’s growth.

However, the industry faces a range of challenges related to human resource needs, congestion and security, entrance of novel players, soaring fuel prices, ongoing growth in high-speed trains, and rapidly surging customer expectations. To stay relevant and meet long-term needs, the industry must keep on innovating its operating models, discover fresher revenue streams and provide exclusive customer experiences.

Here are some of the major trends impacting the airlines sector:

- Commercial Aviation to Continue Dominating the Market

Commercial aircraft makes up the largest market segment, grabbing over 50% of the total market revenues as of 2018. The commercial airline industry is likely to witness a rise in profits in the offing on account of the soaring demand for new aircraft to cater to the booming air travel. Furthermore, some airlines are replacing their obsolete fleet with brand new fuel-efficient planes.

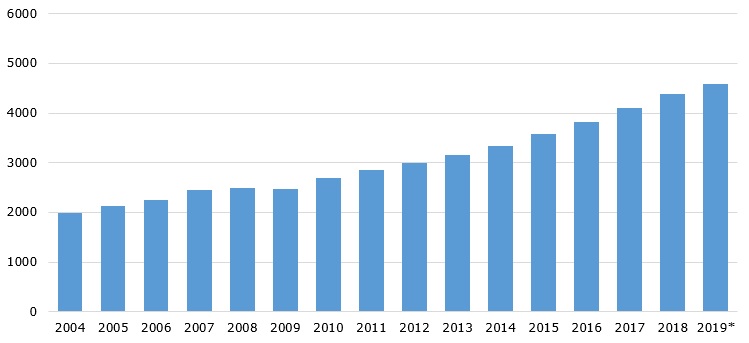

By 2019, the number of scheduled passengers (have booked a flight with a commercial airline) is projected to reach a record level of close to 4.6 billion, about 130% higher as against 2004. In 2017, the APAC region commanded the largest share of airline passenger traffic and also comprises 7 of the 10 most frequented airline routes.

Number of scheduled airline passengers worldwide from 2004 to 2019* (in millions)

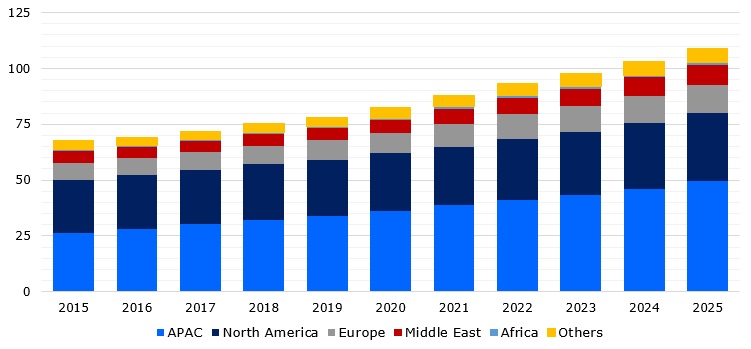

One of the reasons for the continuous air travel growth includes a surge in the number of LCCs, which has recently turned air travel into an inexpensive transport mode. Since 2008, airfares have fallen by around 0.9% on average per annum, largely owing to the intensified competition in the market. Other factors comprise the booming middle class worldwide (especially in China), and the increased investment in airport infrastructure from pole to pole led by the APAC region, causing a stronger load-carrying capacity.

Global spending on airport infrastructure from 2015 through to 2025 (in USD billion), region-wise

The tourism and aviation sectors keep on enjoying an intrinsic relationship. Successful campaigns for tourism development, thriving e-commerce and the advancement of niche markets have contributed to a hike in air services demand, ending in enhanced connectivity for emerging travel destinations.

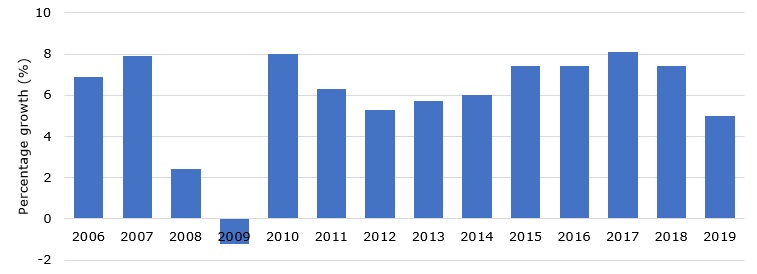

In 2018, the world air traffic passenger demand grew around 7.5% compared to the previous year, whilst that in 2019 is slated to increase with 5% more.

Annual growth (%) in global air traffic passenger demand during 2006-2019*

· Air Companies Require to Resort to Social Media to Build Brand Equity

Like a slew of various major enterprises from pole to pole, some big air carriers have come to explore and use novel ways to interact with customers to enhance their business relationships. This step is important for the airlines to take in case they wish to improve brand equity and grab the mindshare of the current customer.

A number of air companies are very good at utilising social media and social media management (SMM) to draw in new clients and retain the existing ones, whilst others are only starting to do so.

As social media has the advantage in the overall CRM pie, airlines will require to consider creating a robust, large resource pool capable of processing customer requests, complaints, posts and tweets 24 hours a day.

According to the studies performed, nowadays the amount of communication through social media for some of the world's leading air carriers reaches up to 200,000 tweets and nearly 1,000,000 Facebook fans. And over the next while, the figures are poised to see a phenomenal increase. Yet, there is still much to be done before airline companies can really feel confident in managing social media efficiently.

In this regard, it is strategically advantageous for airlines to collaborate with providers that can equip them with a ready-made personnel reserve of social media professionals and technological platforms that help drive stronger brand equity on social networks.

- Smart Convergence of Both Online and Offline Channels is Central to Success

Nowadays, the Internet, embodied by online tourist agencies and airline websites, serves as a potent source of revenue for air companies. Nearly 75% of flights tickets nowadays are purchased online. E-commerce (also termed internet commerce) and workflow automation like web check-in services have made air travel much more convenient. Additionally, the smartphone’s soaring popularity is set to actively participate in CRM and income-earning in the near term.

Yet, against this background, the offline channel or the customer service contact centre is anticipated to keep on being a vital tool of cooperation between the air carriers and the passengers, given the individual approach it imports.

Meantime, on several occasions, clients cease purchasing flight tickets or tour packages on the Internet as a result of slow website loading time, technical errors, or at the time of the billing process utilising different bank cards. Such clients can be retained by the sophisticated mix of both online and offline channels.

And in unforeseen situations, the offline channel, represented by the customer service contact centre, can naturally take the place of the online one to solve customers’ requests or problems.

- Analytics is Gaining Prominence in the Airline Domain

The huge bunch of data generated in the two channels at the breakneck speed encloses very crucial information on passenger profiles, tastes and preferences that can be exploited by air companies in versatile ways, such as offerings of novel products, monitoring of challenges encountered by clients and provisioning of custom solutions, prediction of customers’ desires and tastes by analysing historical data as well as effectively cross- and/or upselling of extra goods/services.

In this context, analytics emerges as a great strategic tool for the airline sector, taking on significance as social media analytics, speech analytics for contact centres and also revenue-raising model analytics.

Analytics provides the airlines industry with key insights, in a way, analytics is turning into an 'altimeter' that will help the business stay on top.

- Altering Strategies to Increase Revenue

Unexpectedly soaring fuel costs, slower economic activity and intensifying competition are factors that are hindering the revenue growth of the world’s airlines industry. Thus, airliners are investigating novel strategies and tapping additional revenue-producing sources such as selling extra products and services in the value chain, among others.

Ancillary services are the vital revenue generator for airlines these days, with the most sought-after of them being charges for checked-in baggage, reserving a preferred seat and Wi-Fi connectivity. To tackle an issue of revenue loss, carriers must examine a total revenue integrity program that touches upon manifold processes encompassing ticketing processes, electronic ticketing, departure control, and CRM.

- Increasing Emphasis on Regulations and Standardisation

Standardisation regulations and policies are expected to keep on dominating the airline domain currently and in the long term. Most of these deal with accounting and finance, environment and rights of consumers.

On the one hand, regulation encourages better passenger safety and more sustainable business, while on the other hand, compliance bumps up the total operation costs that airlines must meet singlehandedly without sharing them with passengers. In view of the introduction of novel regulations for the world airlines industry, air companies must be involved in a compliance program that can be cost-effective, help optimise business processes and modify operations.

- Technological Progress as Important Driver of Aviation Market Growth

The implementation of AI in aviation is slated to skyrocket at a 46.4% CAGR through to 2023, which is set to have an impact on all industry areas. Some air carriers and airports have already introduced AI-based products, like chatbots and virtual helpers. The issue right now is in whether this technology can radically change client service and optimise efficiency.

From 2019, in-flight e/m-commerce solutions such as SKYdeals and AirFree can possibly make duty-free trolleys obsolete. These marketplaces are pioneers in serving customers in the air. For instance, SKYdeals will provide all connected passengers with access to a catalogue of last-minute offers on various service services depending upon their destination, along with an assortment of products at discounted rates (up to 50%). Orders can be delivered home, collected at the arrival gate or issued on mobile devices.

The government of Hainan, the southern province of China, has allowed to provide unlimited Internet access to foreigners and has agreed to lift all limits on FDI in airlines.

Furthermore, 34% of airports worldwide are mulling over blockchain R&D programmes by end-2021. This is deemed to help enhance processes of identifying passengers, to an extent by lowering the need for manifold ID checks.

© MarketPublishers.com, 2019

Key Trends Shaping Global Aviation Industry

The worldwide aviation industry offers services to apparently any part of the globe and is also part and parcel of the world economy. It incorporates suppliers of air transport services for passengers and cargo alike. These services are used by individuals and organisations as well as governmental bodies from pole to pole.

Nowadays, the world aviation industry comprises above 2000 air companies that operate over 23,000 aircraft, rendering service to more than 3700 airports. The coming 20 years will require around 30,050 airplanes with their total value standing at over USD 5.6 trillion.

The aviation market is witnessing fast-paced growth worldwide and is projected to reach USD 832.8 billion in 2020 posting a 3.7% CAGR. Increased defense spending, largely from the developing nations, is likely to drive the procurement of combat aircraft, thereby boosting the aviation sector growth on the immediate horizon. Further, the urge for increased connectivity in today’s global economy, thriving tourism sectors, ongoing demand for new low-cost carriers (LCCs) and deregulation, growing disposable income of the middle-class in emerging markets have contributed a lot to an upsurge in the frequency of air travel and, thus, the aviation industry growth, especially in Asia and the Middle East. This has urged the aviation authorities and air carriers to take efforts with respect to investments in airport infrastructure, route expansions and provisioning of new aircraft deliveries resulting in additional seats. The replacement of old commercial airliners with brand new ones are also amid the key factors igniting the sector’s growth.

However, the industry faces a range of challenges related to human resource needs, congestion and security, entrance of novel players, soaring fuel prices, ongoing growth in high-speed trains, and rapidly surging customer expectations. To stay relevant and meet long-term needs, the industry must keep on innovating its operating models, discover fresher revenue streams and provide exclusive customer experiences.

Here are some of the major trends impacting the airlines sector:

· Commercial Aviation to Continue Dominating the Market

Commercial aircraft makes up the largest market segment, grabbing over 50% of the total market revenues as of 2018. The commercial airline industry is likely to witness a rise in profits in the offing on account of the soaring demand for new aircraft to cater to the booming air travel. Furthermore, some airlines are replacing their obsolete fleet with brand new fuel-efficient planes.

By 2019, the number of scheduled passengers (have booked a flight with a commercial airline) is projected to reach a record level of close to 4.6 billion, about 130% higher as against 2004. In 2017, the APAC region commanded the largest share of airline passenger traffic and also comprises 7 of the 10 most frequented airline routes.

Number of scheduled airline passengers worldwide from 2004 to 2019* (in millions)

One of the reasons for the continuous air travel growth includes a surge in the number of LCCs, which has recently turned air travel into an inexpensive transport mode. Since 2008, airfares have fallen by around 0.9% on average per annum, largely owing to the intensified competition in the market. Other factors comprise the booming middle class worldwide (especially in China), and the increased investment in airport infrastructure from pole to pole led by the APAC region, causing a stronger load-carrying capacity.

Global spending on airport infrastructure from 2015 through to 2025 (in USD billion), region-wise

The tourism and aviation sectors keep on enjoying an intrinsic relationship. Successful campaigns for tourism development, thriving e-commerce and the advancement of niche markets have contributed to a hike in air services demand, ending in enhanced connectivity for emerging travel destinations.

In 2018, the world air traffic passenger demand grew around 7.5% compared to the previous year, whilst that in 2019 is slated to increase with 5% more.

Annual growth (%) in global air traffic passenger demand during 2006-2019*

· Air Companies Require to Resort to Social Media to Build Brand Equity

Like a slew of various major enterprises from pole to pole, some big air carriers have come to explore and use novel ways to interact with customers to enhance their business relationships. This step is important for the airlines to take in case they wish to improve brand equity and grab the mindshare of the current customer.

A number of air companies are very good at utilising social media and social media management (SMM) to draw in new clients and retain the existing ones, whilst others are only starting to do so.

As social media has the advantage in the overall CRM pie, airlines will require to consider creating a robust, large resource pool capable of processing customer requests, complaints, posts and tweets 24 hours a day.

According to the studies performed, nowadays the amount of communication through social media for some of the world's leading air carriers reaches up to 200,000 tweets and nearly 1,000,000 Facebook fans. And over the next while, the figures are poised to see a phenomenal increase. Yet, there is still much to be done before airline companies can really feel confident in managing social media efficiently.

In this regard, it is strategically advantageous for airlines to collaborate with providers that can equip them with a ready-made personnel reserve of social media professionals and technological platforms that help drive stronger brand equity on social networks.

· Smart Convergence of Both Online and Offline Channels is Central to Success

Nowadays, the Internet, embodied by online tourist agencies and airline websites, serves as a potent source of revenue for air companies. Nearly 75% of flights tickets nowadays are purchased online. E-commerce (also termed internet commerce) and workflow automation like web check-in services have made air travel much more convenient. Additionally, the smartphone’s soaring popularity is set to actively participate in CRM and income-earning in the near term.

Yet, against this background, the offline channel or the customer service contact centre is anticipated to keep on being a vital tool of cooperation between the air carriers and the passengers, given the individual approach it imports.

Meantime, on several occasions, clients cease purchasing flight tickets or tour packages on the Internet as a result of slow website loading time, technical errors, or at the time of the billing process utilising different bank cards. Such clients can be retained by the sophisticated mix of both online and offline channels.

And in unforeseen situations, the offline channel, represented by the customer service contact centre, can naturally take the place of the online one to solve customers’ requests or problems.

· Analytics is Gaining Prominence in the Airline Domain

The huge bunch of data generated in the two channels at the breakneck speed encloses very crucial information on passenger profiles, tastes and preferences that can be exploited by air companies in versatile ways, such as offerings of novel products, monitoring of challenges encountered by clients and provisioning of custom solutions, prediction of customers’ desires and tastes by analysing historical data as well as effectively cross- and/or upselling of extra goods/services.

In this context, analytics emerges as a great strategic tool for the airline sector, taking on significance as social media analytics, speech analytics for contact centres and also revenue-raising model analytics.

Analytics provides the airlines industry with key insights, in a way, analytics is turning into an 'altimeter' that will help the business stay on top.

· Altering Strategies to Increase Revenue

Unexpectedly soaring fuel costs, slower economic activity and intensifying competition are factors that are hindering the revenue growth of the world’s airlines industry. Thus, airliners are investigating novel strategies and tapping additional revenue-producing sources such as selling extra products and services in the value chain, among others.

Ancillary services are the vital revenue generator for airlines these days, with the most sought-after of them being charges for checked-in baggage, reserving a preferred seat and Wi-Fi connectivity. To tackle an issue of revenue loss, carriers must examine a total revenue integrity program that touches upon manifold processes encompassing ticketing processes, electronic ticketing, departure control, and CRM.

· Increasing Emphasis on Regulations and Standardisation

Standardisation regulations and policies are expected to keep on dominating the airline domain currently and in the long term. Most of these deal with accounting and finance, environment and rights of consumers.

On the one hand, regulation encourages better passenger safety and more sustainable business, while on the other hand, compliance bumps up the total operation costs that airlines must meet singlehandedly without sharing them with passengers. In view of the introduction of novel regulations for the world airlines industry, air companies must be involved in a compliance program that can be cost-effective, help optimise business processes and modify operations.

· Technological Progress as Important Driver of Aviation Market Growth

The implementation of AI in aviation is slated to skyrocket at a 46.4% CAGR through to 2023, which is set to have an impact on all industry areas. Some air carriers and airports have already introduced AI-based products, like chatbots and virtual helpers. The issue right now is in whether this technology can radically change client service and optimise efficiency.

From 2019, in-flight e/m-commerce solutions such as SKYdeals and AirFree can possibly make duty-free trolleys obsolete. These marketplaces are pioneers in serving customers in the air. For instance, SKYdeals will provide all connected passengers with access to a catalogue of last-minute offers on various service services depending upon their destination, along with an assortment of products at discounted rates (up to 50%). Orders can be delivered home, collected at the arrival gate or issued on mobile devices.

The government of Hainan, the southern province of China, has allowed to provide unlimited Internet access to foreigners and has agreed to lift all limits on FDI in airlines.

Furthermore, 34% of airports worldwide are mulling over blockchain R&D programmes by end-2021. This is deemed to help enhance processes of identifying passengers, to an extent by lowering the need for manifold ID checks.

Analytics & News