Cobalt Market to Get Hotter Spurred by Mounting Demand

23 Oct 2018 • by Natalie Aster

LONDON – Cobalt is one of the most significant metals of the 21st century. Many countries view it as a strategic metal because it is critical to a wide range of industrial applications and essential for modern, sophisticated technologies. Moreover, this metal is not going to be replaced anytime soon. Strong demand along with limited supply has resulted in remarkable gains for the cobalt market this year, and the future outlook is very promising.

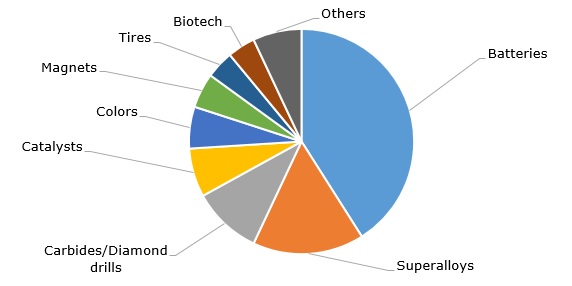

Presently, batteries present the largest application sector for cobalt, accounting for appr. 41% of the world’s cobalt demand. When added to nickel-metal hydride and lithium-ion batteries, cobalt helps to improve its efficiency and stability and also tackle such problems as corrosion, battery explosions, and reduced life cycle. The surging demand for mobile devices (smartphones, tablets, laptops, etc.), electric vehicles and large-format rechargeable batteries acts as the major growth engine of the cobalt consumption.

Another important end-use sector of cobalt in the production of high-strength, wear-resistant, magnetic superalloys which grab a share of around 16% of the overall demand for cobalt. Carbides and diamond drills present the third biggest application of cobalt with a share of nearly 10% of the world’s demand.

Structure of global demand for cobalt by end-uses, 2018

Today, only 2% of the world’s total cobalt output come from primary cobalt production, whilst around 60% are sourced as a by-product from copper mines and 38% - from nickel mines.

The volume of the global cobalt production demonstrated continued growth during 2013-2015 and climbed to 126,000 metric tons as of 2015. However, it experienced a moderate decline in 2016 and totaled some 123,000 metric tons. In the year 2017, the world’s cobalt production volume continued following a downward trend and decreased to 110,000 metric tons.

World’s cobalt mine production during 2008-2017 (in thousand metric tons)

.jpg)

Globally, DR Congo tops the list of the world’s leading cobalt producers by a large margin outpacing other producing countries. Congo grabs a 58.5% share of the world’s total mine production of cobalt. In 2017, the volume of the cobalt mine production in Congo run to about 64,000 metric tons, registering a slight YoY decline. In the wake of the rising demand for cobalt, more attention is given to Congo as cobalt mining in this country is associated with human right abuses and horrible working conditions. However, despite all challenges faced by the country’s cobalt industry, Congo will continue attracting significant amounts of foreign investments in the foreseeable future due to high-quality of minerals mined in the country and low production costs.

Top 10 countries in world’s cobalt mine production during 2015-2017 (in thousand metric tons)

.jpg)

Russia ranks the second leading cobalt mining country in the world. Russia’s cobalt mine production was reached 5,600 metric tons in 2017, which is equivalent to appr. 5.14% of the world’s total output. With concerns regarding cobalt mining in Congo running high, the demand for cobalt from Russia could receive a considerable boost in the coming years – the only question is whether Russia will be able to satisfy the mushrooming demand. Whilst the country’s cobalt reserves are estimated at nearly 250,000 metric tons, Russia still remains well behind Congo in terms of cobalt production.

The third sport on the list of the world’s dominating mine producers of cobalt is held by Australia, accounting for a share of appr.4.59% of the global output. The country’s mine production of cobalt come to around 5,000 metric tons in 2017. The Australian cobalt industry is also receiving more attention from investors in the wake of the increasingly challenging environment in Congo.

COBALT MARKET FUTURE OUTLOOK

The increasing number of cobalt uses along with shifting market forces has resulted in a breathless rally in the value of cobalt. Besides, both soaring demand and mounting concerns over a global supply shortage have prompted the cobalt market to tighten substantially during the recent past, which in turn has heated up cobalt prices. However, on the back of the cobalt prices easing this year, questions have arisen whether the cobalt rally is eventually over; but, the production/consumption balance expected for the coming years suggests otherwise.

With demand from the key end-use industries (especially lightweight electric vehicles, medical, aerospace, electronics, amid others) poised to keep on rising at a brisk pace, and the demand from the battery application slated to see double-digit growth in the next 10 years, the world’s cobalt market is anticipated to enjoy an unprecedented upturn. By the year 2030, the world’s cobalt demand could be more than 45 times higher than it was in the year 2017. Meantime, the global cobalt market is projected to witness further tightening on the supply side. Therefore, whilst the demand for cobalt ramps up and supply struggles to keep up with consumption – an increasing supply/demand gap is expected to emerge, by the year 2021 it could reach 12,000 metric tons. If such a deficit will materialize in the coming years, cobalt prices will likely rise sharply.

© MarketPublishers.com, 2018

Analytics & News