Vegetable Oils Market: Key Facts & Statistics

27 Jul 2018 • by Natalie Aster

LONDON – The world’s market for vegetable oils has exhibited a sustainable growth at a CAGR of around 4% during the last several years and is set to keep on rising in the future supported by steady population growth, changing lifestyles, constantly improving dietary habits, and enhancing awareness amid consumers about health benefits of vegetable oils consumption (e.g., enhanced metabolism, prevention of certain diseases, etc.). Surging trend for natural/organic products along with the ever-greater health consciousness amid consumers also propels an upturn in the vegetable oils market. Other important factors propelling the market growth comprise the mounting demand from the developing countries, flourishing food sector, and rising living standards. However, the vegetable oils market is restrained by a range of challenges like the expanding availability of counterfeit products and diminishing land area for oilseeds.

The APAC vegetable oils market is the largest one worldwide, followed by the European vegetable oils market.

PRODUCTION

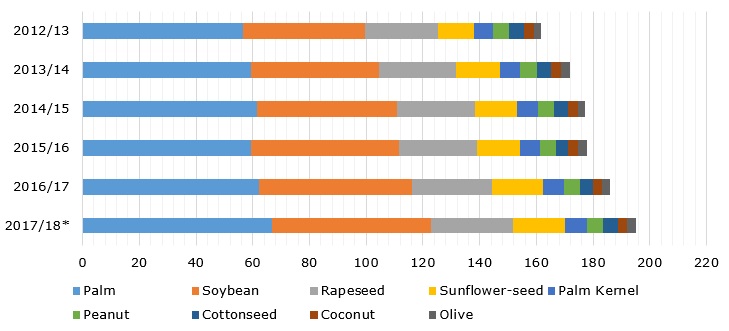

Globally, the production of vegetable oils maintained a modest but steady growth pace for over 10 last years, except the crop year 2014/15 when it registered a slight decline. In 2016/17, the volume of the world’s vegetable oils production added more than 8 million metric tons (MMT) and run to 185.76 MMT. It is anticipated to grow by nearly 9.35 MMT in this crop year to reach new heights exceeding 195 MMT.

World’s vegetable oils production over 2012/13 – 2017/18*, by type (in MMT)

As for types, palm, soybean, rapeseed, and sunflower-seed oils are the top four vegetable oils in terms of production. In 2016/17, their combined production volume was above 162.2 MMT. By the end of 2017/18, it is anticipated to surpass 169.9 MMT.

Presently, palm oil represents the biggest oil type accounting for 32% of the overall vegetable oils output. Its production volume was over 62.3 MMT in 2016/17 and is set to go beyond 66.8 MMT this crop year. Indonesia is the unrivaled producer of palm oil, grabbing a share of more than 60% of the world’s total volume of the palm oil production. It is followed by Malaysia with a share of 32%. Other less prominent palm oil producers comprise Thailand, Colombia, and Nigeria; together they account for a share of nearly 8.4%.

The second biggest sector of the vegetable oils market is soybean oil, which captures a share of appr. 28% of the world’s total production volume of vegetable oils. In 2016/17, the global volume of soybean oil output gained nearly 1.95 MMT and climbed to 53.94 MMT. By the end of the current crop year, it is set to come over 56.1MMT. China, the US, and Argentina are the top three soybean oil producers globally; in 2016/17 the volume of the soybean oil production in these countries reached 15.77, 10.04, and 8.55 MMT, respectively.

Rapeseed oil takes the third position in the vegetable oils market in terms of production. Last crop year, the output volume of rapeseed oil exceeded 28.1 MMT. It is poised to go beyond 28.7 MMT in 2017/18. Canada, Germany, China, and India are amid the top rapeseed oil producing countries.

CONSUMPTION

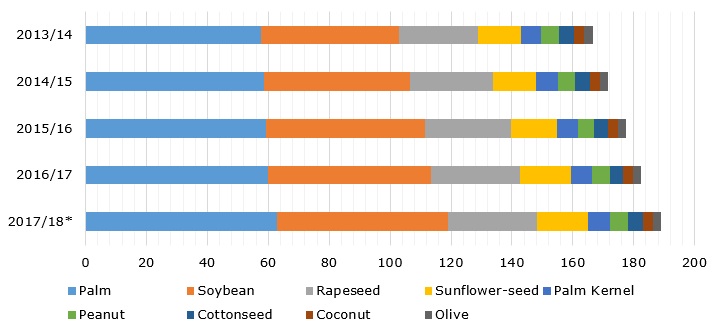

From pole to pole, the consumption of vegetable oils witnessed a steady increase during the past several years spurred by the rising global population along with the growing appetite for vegetable oils from the key end-use applications. In the crop year 2016/17, estimated 182.3 MMT of vegetable oils were consumed worldwide. By the end of the current crop year, the world’s volume of the vegetable oils consumption slated to cross 189 MMT.

World’s vegetable oils consumption over 2013/14 – 2017/18*, by type (in MMT)

Palm, soybean, rapeseed, and sunflower-seed oils are the most-consumed types of vegetable oils worldwide. Globally, there were consumed around 59.97 MMT of palm oil, 53.62 MMT of soybean oil, 29.22 MMT of rapeseed oil, and 16.52 MMT of sunflower-seed oil.

The Food industry holds a bulk share of the overall vegetable oils consumption. The escalating demand for vegetable oils owing to their desirable qualities (like low-cholesterol, low-fat, and low-calorie content) and the increasing need for healthy, organic, and natural cooking oils in the wake of the surging health and food safety concerns are expected to encourage further expansion of vegetable oils usage in the Food industry.

However, besides being edible, vegetable oils find numerous industrial applications: they are used in the manufacturing of cosmetics, soaps, paints, detergents, lubricants, candles, etc. Moreover, the biofuels sector has emerged as a promising end-use of vegetable oils which is gaining momentum at the highest pace.

EXPORTS

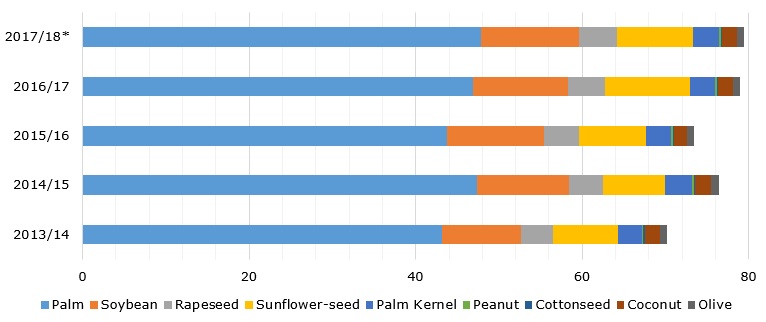

After a decline in the crop year 2015/16, the global exports of vegetable oils came up by above 5.5 MMT and reached almost 79 MMT. Palm, soybean, sunflower-seed, and rapeseed oils are the top four traded oils worldwide.

World’s vegetable oils exports over 2013/14 – 2017/18* (in MMT), by type

Globally, the overall palm oil exports went beyond 46.8 MMT in 2016/17 and is expected to go beyond 47.8 MMT this crop year. Indonesia is the dominant palm oil exporter with a share of nearly 55.5% of the world’s total export volume. The second biggest palm oil exporter is Malaysia capturing a share of 29%. Other palm oil exporting countries (including the Netherlands, Guatemala, Colombia, Papua New Guinea, amid others) account for tiny shares in global exports.

The global soybean oil exports witnessed a moderate decline of appr. 240,000 metric tons in 2016/17 and totaled 11.4 MMT. It is forecast to grow to 11.75 MMT in 2017/18. Argentina, Brazil, and the US are the top three soybean oil exporters globally. The leading exporter – Argentina, exported around 5.45 MMT of soybean oil in 2016/17.

The export volume of the third most-exported vegetable oil – sunflower-seed oil, surpassed 10.2 MMT, registering YoY growth by over 2.1 MMT. In 2017/18, the export volume of sunflower-seed oil is predicted to decrease to 9.21 MMT. Ukraine is the dominant sunflower-seed oil exporter worldwide, this country exported appr. 5.85 MMT of sunflower-seed oil in 2016/17. It is followed by Russia with the sunflower-seed export volume of above 2.17 MMT in the past crop year.

The fourth spot on the list of most-exported vegetable oils is held by rapeseed oil. The world’s volume of rapeseed exports added 350,000 metric tons in 2016/17 and amounted to 4.49 MMT. This crop year, it is set to remain at the same level. Canada is ranked as the top rapeseed oil exporter in the world.

IMPORTS

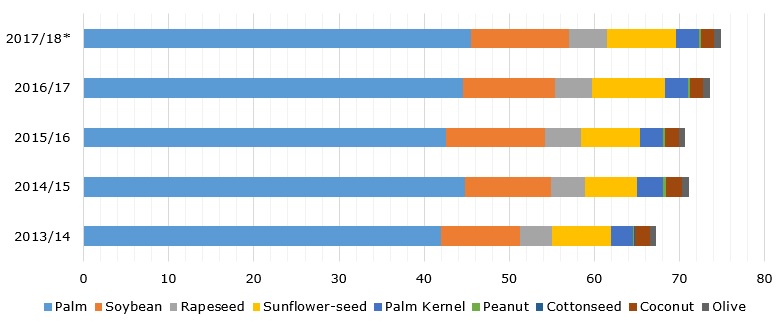

As for global vegetable oils import volume, it registered a moderate increase after a small decline in 2015/16. In the crop year 2016/17, the world’s import volume of vegetable oils climbed to 73.54 MMT. Palm, soybean, sunflower-seed, and rapeseed oils are the most-imported vegetable oils worldwide.

World’s vegetable oils imports over 2013/14 – 2017/18* (in MMT), by type

Worldwide, the palm oil import volume reached 44.51 MMT in 2016/17 and is poised to touch 45.5 MMT in 2017/18. The countries with substantial volumes of palm oil imports include India, China, Pakistan, Bangladesh, the Netherlands, Italy, and Germany, amidst others.

The world’s soybean oil imports registered a decline by 770,000 metric tons in 2016/17 and was estimated at around 10.86 MMT. It is expected to add 620,000 metric tons and reach 11.48 MMT in 2017/18. The major import destinations of soybean oil include India, Bangladesh, China, Algeria, Morocco, Iran, and Venezuela, amidst others.

The global import volume of sunflower-seed oil is slated to come down from appr. 8.58 MMT in 2016/17 to 8.08 MMT in 2017/18. The leading sunflower-seed oil importers are India, Turkey, China, Spain, the Netherlands, Italy, and Germany.

Worldwide, the rapeseed import volume was about 4.37 MMT in the past crop year. It is projected to grow by 160,000 metric tons in the crop year 2017/18. The biggest volumes of rapeseed imports go to such countries as China, the US, the Netherlands, Belgium, Norway, Germany, and the Czech Republic.

© MarketPublishers.com, 2018

Analytics & News