Coffee Market: Current Scenario across Top-Producing Countries

28 May 2018 • by Natalie Aster

LONDON – Every morning coffee is energizing millions of people across the globe. Coffee is the third most consumed beverage (after water and tea). It is the second most traded commodity worldwide, outpaced only by oil. Furthermore, coffee makes up a fundamental part of food culture in many countries. Coffee consumption has long ceased to be just a daily ritual (from having a cup at home to one on the go), it has become a vital part of modern people’s lifestyle.

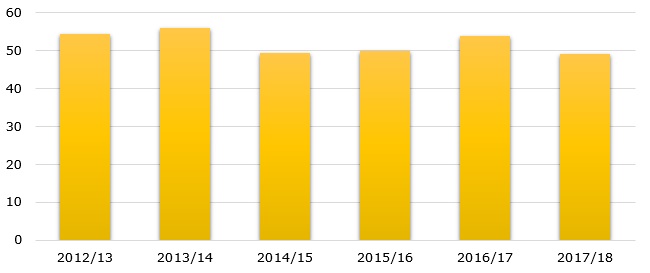

The global consumption of coffee has experienced a modest but steady growth in the last few years. In the crop year 2016/17, the global volume of coffee consumption remained almost unchanged and was estimated at around 155.1 million 60-kg. bags. It is anticipated to climb to 157.6 million 60-kg. bags in 2017/18.

Worldwide coffee consumption during 2012/13 – 2016/17 (in million 60-kg. bags)

Along with the constantly growing consumption of coffee, the world’s coffee industry continues to follow an upward trend. Growth in the coffee market is propelled by the elevating number of coffee drinkers from pole to pole, enhancing popularity of out-of-home coffee drinking, increasing urban population, surging coffee sales via online retailing, and rising disposable incomes of consumers. Asia-Pacific is the leading revenue contributing region in the global coffee market.

In the crop year 2016/17, the world’s output of coffee demonstrated a 3.4% YoY increase and totaled 157.44 million 60-kg. bags, majorly owing to an upturn in the Honduran coffee production. The world’s coffee production is anticipated to climb to 158.9 million 60-kg. bags, registering a 0.8% YoY gain.

Global coffee production during 2003/04 – 2017/18 (in million 60-kg. bags)

.jpg)

Owing to the rising coffee production against stable consumption, the world’s coffee market registered a surplus in 2016/17 after 2 consecutive years of deficit: production exceeded consumption by slightly over 2.3 million 60-kg. bags.

As for source types, the coffee market is segmented into Arabica (capturing a 70% market share), Robusta (27%) and Liberica (3%). The Arabica production is set to fall by 1.1% YoY and total nearly 97.32 million 60-kg. bags in the 2017/18 crop year owing to an expected decline in output from Brazil and Colombia. Meantime, Robusta production is projected to see healthy YoY growth by around 3.75% in this crop year, largely due to a rebound in Vietnam’s market, and is poised to amount to 61.46 million 60-kg. bags.

As for regional coffee output in the 2017/18 crop year, Africa is forecast to see a 4.7% YoY increase, Asia & Oceania will likely go up by 5.9% YoY, and Mexico & Central America are set to rise by 7.1% YoY. Meantime, the coffee output volume in South America is poised for a 4.9% YoY decline.

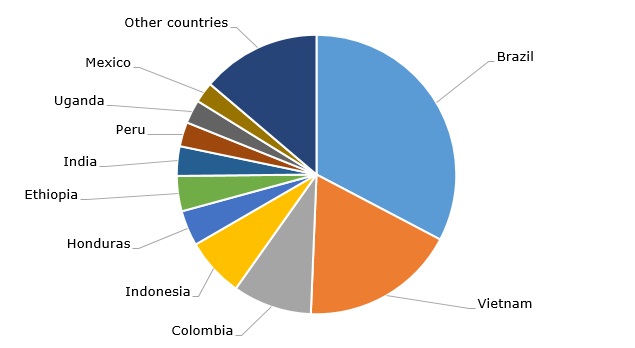

The bulk share of the world’s coffee output comes from the developing world. Top coffee-producing nations include Brazil, Vietnam, Colombia, Indonesia, Honduras, amidst others.

Top coffee-producing countries, 2017

BRAZIL

Globally, Brazil has been maintaining the leading position in terms of coffee output for more than 150 years, contributing around one-third of the world’s total production of coffee. The country is also the top exporter of coffee in the world, the major export destinations comprise the US, Germany, Belgium, Italy, and Japan.

In 2017, Brazil’s coffee market suffered from insect infestation and unfavourable weather conditions, this is supposed to negatively affect the country’s Arabica production (it will likely fall by around 7%) and total coffee output in 2017/18. Meantime, Brazil’s Robusta output volume is set to add 1.1% in 2017/18.

Nearly 90% of Robusta beans produced in Brazil are used domestically in the national instant-coffee industry. The current lack of coffee supply in Brazil has pushed the international prices to soar to a 5-year high. Therefore, in the wake of the escalating Robusta prices, the country’s government is planning to import around 60,000 tonnes of green Robusta beans. Whilst earlier Brazil used to import roasted and ground coffee, the necessity to import green coffee beans hasn’t arisen for about 200 years.

Brazil coffee production during 2012/13 – 2017/18 (in million 60-kg. bags)

By late 2018, Brazil’s revenue generated in the coffee sector is likely to exceed USD 8.8 billion. Furthermore, it is expected to rise at a 5.4% CAGR through 2021. The US is the top revenue contributor to the Brazilian coffee market, accounting for around 22% of the Brazilian exports.

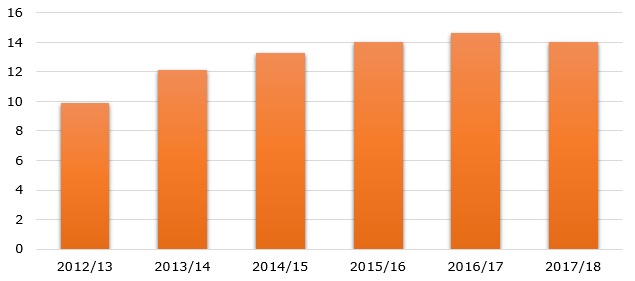

VIETNAM

The world’s second-biggest producer of coffee is Vietnam. During, the past few decades, the coffee industry in Vietnam has developed as a key export-oriented industry. Today, appr. 90-95% of the Vietnamese coffee output are exported, annually bringing billions of USD in revenue. Besides, Vietnam ranks the top grower of Robusta worldwide.

Owing to poor weather conditions, the Vietnamese output of coffee dropped by nearly 11.1% in the crop year 2016/17. However, it is set to rebound in 2017/18 and add 11.6%, totaling around 28.5 million 60-kg. bags at the end of this crop year.

Vietnam coffee production during 2012/13 – 2017/18 (in million 60-kg. bags)

In the wake of the mounting production, Vietnam’s coffee shipments may surge this year, as local farmers harvest a bigger crop. In 2018, the country’s coffee exports may reach 1.55 million metric tonnes.

By late 2018, revenue of the Vietnamese coffee industry is predicted to surpass USD 1.29 billion. Through 2021, the country’s market is poised to see a 13.7% CAGR. The major importer of the Vietnamese coffee in the US.

Though Vietnam’s coffee industry has fared well during the recent years since the domestic production has skyrocketed, the prosperity is threatened by environmental limitations, looming climate and certain structural challenges.

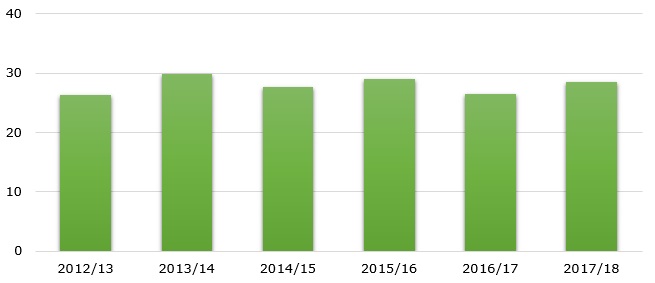

COLOMBIA

Colombia is the third largest producer on the world’s coffee arena. Traditionally, it was second after Brazil but has moved to the third place owing to the robust expansion of the Vietnamese coffee market.

The Colombian coffee production witnessed a steady, modest upturn during the 2012/13 – 2016/17 crop years. In the last crop year, Colombia harvested 14.6 million 60-kg. bags.

Colombia coffee production during 2012/13 – 2017/18 (in million 60-kg. bags)

Excessive rain has led to a lower output of coffee in Colombia in Q1 of the current crop year, therefore the country’s overall production volume is likely to fall by 4.3% YoY and total around 14 million 60-kg. bags at the end of the current crop year.

Over the last twelve months (April 2017 – March 2018), the Colombian coffee exports decreased by nearly 2% and reached 12.8 million 60-kg. bags.

Conclusion

Coffee has become an integral part of modern lifestyle. Around half a trillion cups of coffee are consumed worldwide every year. With a café at every turn in many cities across the world, it’s not surprising that coffee is among top consumed beverages and most traded commodities in the world. The leading producing countries each annually harvest millions of kilograms of coffee beans that further find their way to eager consumers.

© MarketPublishers.com, 2018

Analytics & News