Hungarian Construction Market to Recover in 2013-2014, Finds PMR

27 Jul 2012 • by Natalie Aster

After a poor 2009-2012 for the Hungarian construction industry, from 2013 a visible market recovery is expected. The growth in 2013-2014 will result from the intense execution of EU co-financed infrastructure investments as well as some revival in building construction, particularly in non-residential buildings.

According to the PMR’s latest report, entitled “Construction Sector in Hungary 2012”, weak macroeconomic environment, falling investment demand and poor household finances led to the Hungarian construction sector being in recession since 2006. As a result the value of gross value added in construction in 2011 was almost one third lower than in 2005. However, in the last quarter of 2011 the year-to-year decline of value added decelerated to only 1.4%, a direct result of accelerating public investment financed by EU funds. After 2012 the improving macroeconomic condition and higher public investment are likely to finally reverse this negative trend.

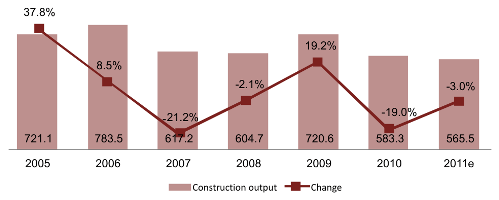

The crisis affected the Hungarian engineering construction sector badly and the main problem is that the government, which is primarily responsible for the construction of transport infrastructure, does not have the budget to finance constructions. Since 2000, when its length was 571 km, the motorway network more than doubled, and in an average year 65 km of new motorway and expressway were completed. 2011 was rather weak and only 31 km opened, and for 2012 we expect another weak year.

As a result, for 2012 we expect an approx. 4% fall in engineering construction output. The 2012 forecast is also supported by the volume index of new orders among engineering companies. In 2011 the volume of new orders decreased by 16% y-o-y. At the beginning of 2012 the volume index shows an increasing trend, so from 2013 and 2014 a slow increase in civil engineering output is expected.

Civil Engineering Construction Output in Hungary (HUF Bn) and Y-O-Y Change (%), 2005-2011

In the coming years car manufacturing will play an important role in Hungary’s industrial construction. Apart from the manufacturing industry, the largest planned project involves the expansion of Hungary’s only nuclear power plant, in Paks. Constructions on the power plant are estimated at €8-10bn. The purpose of the expansion is to increase the capacity of the reactors to serve the growing energy needs of the population. After expansion the reactors would be in operation until 2032-2037.

Report Details:

Construction Sector in Hungary 2012

Published: May, 2012

Pages: 109

Price: US$ 2.240,00

In non-residential construction the industrial and warehouse sector is expected to recover from the crisis first. The wholesale and retail sector will continue to suffer not only from the moderate consumption and as a result of poor demand, but also from the government’s regulation that will prevent the issuing of building permits to many huge retail construction projects until the beginning of 2015. It is unlikely that any large developments will start in 2012. However, it is expected that by 2015 the sector will recover.

Although non-residential investors are not starting any new projects, they are initiating construction works, and many buildings are being modernised and renovated. The signs of recovery will be first visible in 2013, when an increase in output may take place. At the moment, it seems that restoring construction industry’s non-residential sector will be a slow process. The fact that an increase is forecasted for 2013 is also due to non-residential construction output in 2011 and 2012 being already so low that even a slight positive change in the economic atmosphere and business confidence can improve the situation.

More information can be found in the report “Construction Sector in Hungary 2012” by PMR.

To order the report or ask for sample pages contact [email protected]

Contacts

MarketPublishers, Ltd.

Tanya Rezler

Tel: +44 208 144 6009

Fax: +44 207 900 3970

[email protected]

MarketPublishers.com

Analytics & News