Diabetes Market to 2016 - Biguanides and Insulin Analogs will be the Largest Selling Anti-Diabetic Drugs

09 Dec 2010 • by Natalie Aster

The report “Diabetes Market to 2016 - Biguanides and Insulin Analogs will be the Largest Selling Anti-Diabetic Drugs ” by GBI Research provides in-depth analysis of the unmet needs, drivers and barriers that affect the global diabetes therapeutics market. The report analyzes the markets for diabetes in the US, the top five countries in Europe (the UK, Germany, France, Italy and Spain) and Japan. Treatment usage patterns, sales and price are forecast until 2016 for the key geographies as well as the leading therapeutic segments. Further, the report provides competitive benchmarking for the leading companies and analyzes the mergers, acquisitions and licensing agreements that shape the global markets.

Report Details:

Published: December 2010

Pages: 153

Price: USD 3,500

Report Sample Abstract:

The Global Diabetes Market is Lucrative despite the Major Drugs in the Market being Associated with Heart Risks

GBI Research finds that the global diabetes therapeutics market is lucrative despite product failures. The major factor driving the growth of the market is the rising incidence of the diabetes diseased population in key markets such as the US, the UK and Germany.

In 2009 the global diabetes diseased population was estimated at 55.6 million, of which 5.6 million was type 1 diabetes and 50.0 million was type 2 diabetes. In 2009, the type 2 diabetes market accounted for 69% of the global diabetes therapeutics market. The diabetes market has experienced some product failures. Avandia (rosiglitazone), belonging to the class of glitazones, was found to increase the probability of heart complications. Following this, sales decreased from a peak of $3 billion to $1.2 billion in 2009. Actos (pioglitazone hydrochloride), another glitazone, took over the market share from Avandia. However, Actos (pioglitazone hydrochloride) was also found to be associated with an increased risk of heart-related problems. Nevertheless, the diabetes market survived due to the increased utilization of other drugs such as insulin analogs and biguanides. Some promising molecules in the peptide analogs class are expected to be launched in the market in the future.

GBI Research forecasts that the diabetes therapeutics market will grow at 6.1% between 2009 and 2016. The market will be primarily driven by the rising prevalence rates and the market entry of new products such as teplizumab and some new molecules belonging to the peptide analogs class.

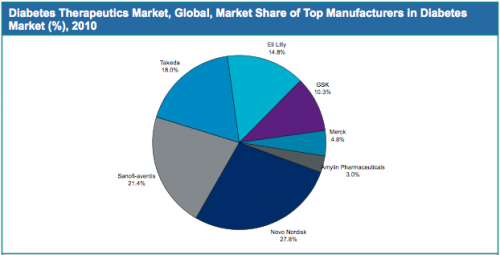

The Global Diabetes Market is Concentrated with the Top Three Companies Accounting for More than 60% of the Market

GBI Research finds the global diabetes therapeutics market to be concentrated, with the top three companies accounting for more than 60% of the market share. Novo Nordisk, Sanofi-Aventis and Takeda are the leading players in the diabetes market. The competitive landscape in the markets is set to change due to the success of recent launches and the potential success of new drugs that will be launched during the period 2009-2016. The market will also be impacted by the decline in sales of leading products such as GSK’s Avandia and Takeda’s Actos. GBI Research estimates that the market share of Eli Lilly and Merck in the diabetes market will increase due to the potential success of teplizumab, which is in Phase III, and Januvia(sitagliptin), which was launched in 2006 and has increased sales exponentially ever since. In addition, Novo Nordisk’s Victoza (liraglutide) is expected to give tough competition to Merck’s Januvia and generate sales of $1.4 billion by 2014 for the company.

Licensing and Mergers and Acquisitions Strategy will Help Companies to Meet the Unmet Need in the Market

GBI Research indicates that the diabetes therapeutics Mergers and Acquisition (M&A) landscape is moderately active since only a few major pharmaceutical companies and medium players are looking for strategic partnerships with companies that have promising drugs either in the pipeline or in the market. In 2009-2010, a total of 48 M&A and licensing deals took place. The diabetes market is dominated by insulins. However, there is a need for products that are easy to administer. This unmet need and the growth potential are driving the deals activity in the industry. The major acquisition activity that took place between 2008 and 2010 includes Daiichi Sankyo’s acquisition of a majority stake in Ranbaxy in November 2008 and the acquisition of OSI Pharmaceuticals by Astellas Pharma in June 2010. The acquisition considerably added to the pipeline potential of these companies in the diabetes market. Licensing activities involving approved products such as Januvia and Galvus and Phase III products such as Oral-lyn will impact on the market. GBI Research suggests that the licensing and M&A activity will continue to be an attractive strategy for players to strengthen their market positions.

More information can be found in the report “Diabetes Market to 2016 - Biguanides and Insulin Analogs will be the Largest Selling Anti-Diabetic Drugs ” by GBI Research .

To order the report or ask for sample pages contact [email protected]

Contacts

MarketPublishers, Ltd.

Mrs. Alla Martin

Tel: +44 208 144 6009

Fax: +44 207 900 3970

[email protected]

www.marketpublishers.com

Analytics & News