Increase in Aging Population of Developed Countries Is Driving the Pharmaceutical Industry towards Growth

03 Dec 2010 • by Natalie Aster

MarketPublishers Ltd announces that new report “Pharmaceutical Industry - 2010 Yearbook - Therapeutic Market Landscape, Key Pipeline Drugs, Top Pharma Companies and Key Mergers and Acquisitions” elaborated by GBI Research is available in its catalogue.

The effect of economic recession was evident on the global pharmaceutical industry by its single digit growth in 2009. However, the steady increase in the aging population of developed countries has been driving the global pharmaceutical industry towards growth. Majority of the diseases are age-related and there has been constant increase in their prevalence due to an increase in the aging population. Greater the elderly population, greater will be the diseased population. According to the US census, the population demographics have been dramatically changing with the average age in the US, going up from 45 to 52 years between 1990 and 2005. The general population in the US has grown at 0.88% per year, however, the 65 years and above population has grown at 2.5% per year. The elderly population in the US has grown from 33 to 85 million within the time period 1990 – 2005. This growth rate is driven by 2 major factors: firstly, the baby boomer population is now entering the mid-60’s age group and secondly, the life expectancy of the general population including the elderly age group has increased from 78 to 85 years. As the lifespan of senior citizens increases, more age-related disease and illness is observed in these individuals. A combination of larger pre-disposed elderly population, along with a longer life span will drive the growth in the pharmaceutical industry. The industry will face increased demands driven by the growth in diseased population.

Report Details:

Published: December 2010

Pages: 177

Price: USD 3,500

Report Sample Abstract:

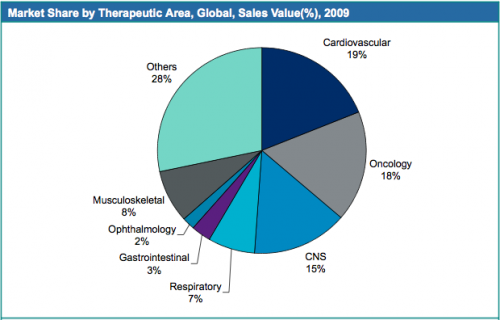

The Cardiovascular, Oncology and Central Nervous System (CNS) Therapeutics Account For More Than 50% of the Total Sales

Cardiovascular, oncology and CNS therapeutics accounted for more than 50% of the total pharmaceutical market by indication. The three therapeutic segments accounted for 52% of the total pharmaceutical market. Cardiovascular disorder therapeutics accounted for 19% of the total market share, closely followed by oncology therapeutics with 18% and CNS therapeutics with 15% of the total pharmaceutical market share. These three major indications contribute the most to the total pharmaceutical market.

The high market share of cardiovascular, oncology and CNS therapeutics indicates that these therapeutic areas will decide the way forward for the global pharmaceutical industry. Majority of the pharmaceutical companies deal in these three therapeutic areas and their endeavour has been to increase and consolidate their portfolio in these therapeutic areas.

Strategic Consolidations by Major Pharmaceutical Companies Are Changing the Global Pharmaceutical Market

Strategic consolidations by major pharmaceutical companies are changing the global pharmaceutical market scenario. The major mergers and acquisitions (M&A) deals of 2009 were acquisition of Wyeth by Pfizer, Genentech by Roche and the merger of Merck and Schering-Plough. The dynamic nature of the pharmaceutical industry is expected to continue because patent expirations of major blockbuster drugs will lead the pharmaceutical companies to consider strategic consolidations to maintain their market position and, to have pipeline drugs. Pharmaceutical companies need to find alternative options to maintain their revenue generation and this can be done by acquiring regional and niche players. It is important for pharmaceutical companies to plan for the long term, so that the slow pace of research and development (R&D) can be objectively managed. The acquisition of small and niche pharmaceutical companies by major pharmaceutical companies show a very dynamic future scenario in the pharmaceutical arena.

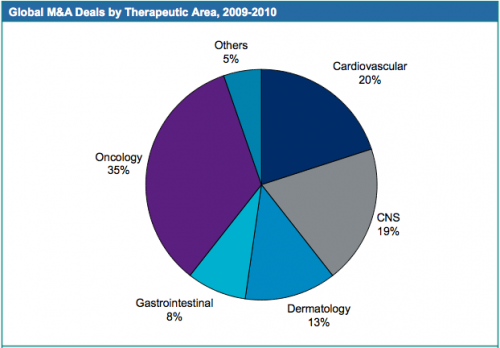

More than 70% of the total value of M&A deals was from oncology, cardiovascular and CNS therapeutics. This indicates the high value of M&A deals in oncology, cardiovascular and CNS therapeutics.

The contribution in M&A deals involving oncology to the total value of M&A deals was 35%. This signifies that the oncology therapeutics area witnessed M&A deals of the highest value. This was followed by cardiovascular and CNS therapeutics contributing 20% and 19% respectively to the total value of M&A deals.

More information can be found in the report “Pharmaceutical Industry - 2010 Yearbook - Therapeutic Market Landscape, Key Pipeline Drugs, Top Pharma Companies and Key Mergers and Acquisitions” by GBI Research.

To order the report or ask for sample pages contact [email protected]

Contacts

MarketPublishers, Ltd.

Mrs. Alla Martin

Tel: +44 208 144 6009

Fax: +44 207 900 3970

[email protected]

www.marketpublishers.com

Analytics & News