Data Centre Market in Central & Eastern Europe is Booming, According to PMR

08 May 2012 • by Natalie Aster

Forecasts for the data centre market in Central and Eastern Europe are positive. Especially in a short term it would be difficult to assume the market will slow down significantly or decline. Even the constant pressure on prices, which decreases the competitiveness of the local markets compared to Western European and Scandinavian countries, can now do sector almost no harm.

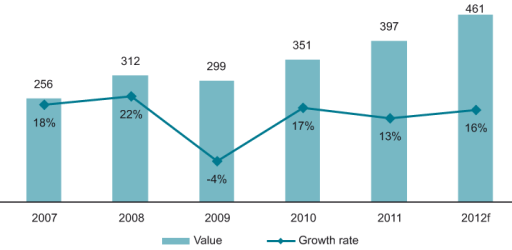

According to the latest report “Data centre market in Central and Eastern Europe 2012” by PMR, the data centre market will continue to grow posting double-digit numbers both in terms of revenues of the market participants and the offered floor space, with the expected growth rate of 16% only in 2012. It is possible that the market may grow even twice as fast, especially that it may be strongly influenced by one-time events and projects which may distort its value significantly.

Value (€ m) and growth rate(%) of the data centre services market in CEE, 2007-2012

It is worth noting that almost all of the major data centre service providers PMR canvassed indicated that they planned to increase their current floor surface in the next one to two years, either by enhancing and rebuilding their current locations or by investing in building facilities in new locations. All in all, PMR assumes that the data centre market will continue to be the market of the seller, with double-figure margins and possibility of investment to increase the current capacity. Over the next three years, approx. 50,000 m2 of data centre floor space for colocation and hosting services will be added in the CEE region. The increasing floor space in data centres, competitive prices and a stable macroeconomic environment will be increasingly encouraging large companies to remove and relocate their server space to the facilities in Central and Eastern Europe. This in turn will positively affect the revenues of the providers.

Major factors influencing the situation on the data centre market in the CEE in the coming years will be: evolution of energy prices, the level of demand for data centre services from the largest clients, growing amount of data transferred within telecommunications networks, growing popularity of online based and cloud services as well as hardware virtualisation services, mergers and acquisitions activity and entrance of new foreign players to the data centre market.

The combined value of the data centre market in Central and Eastern Europe totalled approx. €400m in 2011, which was a growth of 13% in comparison with 2010. After the stagnation observed in 2009, the market maintained the positive double-digit growth rate experienced in 2010. Poland is by far the largest data centre market in CEE, both in terms of net floor surface of commercial data centre facilities as well as combined revenues from data centre services provision. In 2011 a total of 31% of the overall data centre capacity accounted for Poland, followed by the Czech Republic, Hungary, Bulgaria, Romania and Ukraine.

Shares (%) of particular countries in the volume of the commercial data centre net floor surface in CEE, 2011

Report Details:

Data centre market in Central and Eastern Europe 2012

Published: April, 2012

Pages: 163

Price: US$ 3.220,00

The data centre market in CEE has been strongly evolving in the last years, trying to catch up with the global industry trends. At present, the key features of the data centre market in the CEE include:

- in the past tendency to set up small, basic level, and in-house data centre facilities – most requirements are retail colocation focused

- new facilities being constructed to international standards

- data centre services most often provided as an extra to traditional carrier services of telcos

- majority of new supply in the region provided by local domestic data centre operators

- most activity in capital cities (Prague, Budapest and Warsaw)

- fragmented market – but first signs of local consolidation

- limited capital for investment.

More information can be found in the report “Data centre market in Central and Eastern Europe 2012” by PMR.

To order the report or ask for sample pages contact [email protected]

Contacts

MarketPublishers, Ltd.

Tanya Rezler

Tel: +44 208 144 6009

Fax: +44 207 900 3970

[email protected]

MarketPublishers.com

Analytics & News