Retail Markets in All Russian Federal Districts Increased in 2010 by Total $80bn

27 Oct 2011 • by Natalie Aster

In 2010, Russian retail market recovered after the economic slowdown observed in the previous year and increased by 12.6% to RUB 16.4tr ($541bn). However, the latest PMR report „Retail in Russia 2011 - Regional Focus - Market Analysis and Development Forecasts for 2011-2013” shows that particular regional retail markets still reveal differences in their development due to their unique nature and local characteristics. Some companies went bankrupt, the majority had to focus on efficiency rather than dynamic expansion, still, the most prominent of them kept their positions.

After years of dynamic development, Russian retail market experienced a sharp drop in the growth rates, from 28% in 2008 to less than 5% in 2009. In 2010, the retail market in Russia began to reveal signs of recovery after the financial crisis and grew by nearly 13% y-o-y, reaching RUB 16.4tr ($541bn). According to the latest PMR report, each Federal District (Central, Volga, Southern, Siberian, Urals, Northwestern and Far East) enjoyed an increase in the retail sales, of at least 8% reported by the Urals. However, the growth in real terms (4.4%) reveals that last year retail sales were mainly driven by the increase in prices.

Central Federal District again sets the tone for the Russian retail

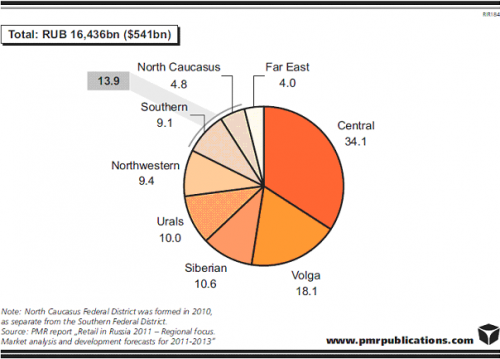

The retail industry in Russia varies significantly among the Federal Districts both in terms of value and the character of development. Being the smallest and the most populous region of Russia, the Central Federal District remains the largest retail market in the country, accounting for 34% of country sales in 2010. The Far East traditionally had the lowest share of retail sales among the Federal Districts in Russia. At the same time, the Far East is the largest District in terms of area with the population that comprises only 6% of Russians.

Retail turnover in Russia by Federal District (%), 2010.

The variations in the retail market development between the regions result from the number of inhabitants, population density, level of urbanisation, as well as average monthly income and expenditures, existing competition and other regional characteristics.

The Central Federal District boasts the lowest unemployment rate (4.4% for the first nine months of 2010), the highest average monthly income per capita ($763) as well as expenditures on goods and services ($529). It is the second urbanised region, with more than 300 cities and the highest population density. It also leads by retail sales per person ($4,970). At the opposite end of the scale there are the newly formed Northern Caucasus Federal District – with 15.9% of the unemployed, monthly income reaching only $410 and expenditures of $308 – as well as the Siberian Federal District, where the level of spending hardly exceeds $300 and retail sales per capita are the lowest among all the districts ($2,926).

Report Details:

Retail in Russia 2011 - Regional Focus - Market Analysis and Development Forecasts for 2011-2013

Published: March 2011

Price: US$ 2,840.00

Southern catches up, Central regains its significance

Considering the pace of retail development in 2010, the Southern Federal District (including the Northern Caucasus) demonstrated the most dynamic sales growth (17%), whereas the Urals experienced the weakest increase in Russia (8%). The Siberian Federal District recovered, after negative development recorded in 2009, and reached 9% growth rate.

The Central Federal District grew by 14%, which also exceeds the country’s average. After the years when the District has been developing at the lower pace than the other ones and as a result has lost its share in the total retail turnover of the country, the financial crisis stopped this trend. Over the last two years, the retail sales in the District have grown stronger compared to total Russia. The majority of the largest retailers in Russia originate from Moscow, which gives the Central Federal District the special status of the region accommodating the leading domestic operators as well as foreign retailers establishing their presence in Russia (as they have tended to start their operations from the country’s capital).

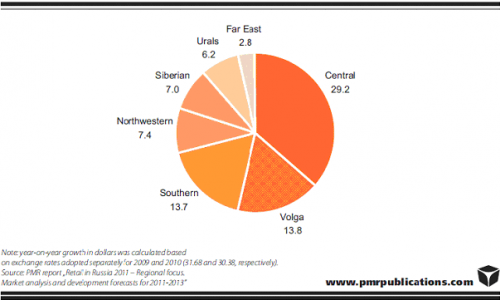

In dollars, retail market in Russia gained 80bn in 2010, of which 60bn excluding an effect of exchange rates. The majority, i.e. more than one-third, was worked out in the Central Federal District. The Southern and Volga Federal Districts contributed to the Russian growth evenly. Owing to these three districts, the Russian retail market gained nearly $57bn in 2010.

Contribution of particular Federal Districts to he retail sales growth in Russia ($bn), 2010.

Winners and losers

Despite certain recovery of the retail market of Russia, in 2010 some international retailers ceased their operations in the country (i.e. Carrefour). In addition, several national retail operators went bankrupt in 2010, for example, the Mir consumer electronics chain. As PMR research shows, the crisis forced most retail operators to focus on the efficiency of their business activity and to cease expansion. Another result of the financial crisis was a change in consumer behaviour, which led, among others, to increased interest in less expensive goods and, as result, a significant growth of popularity of private labels.

The major victims of the financial crisis were the local retail operators, while the leading national players tend to retain their positions on the market on the threshold of increasing competition from foreign retailers. Thus, for example, local grocery retail chains which went bankrupt include Smartkauff in the Volga, V dvukh shagakh in the south of Russia, Samokhval in the Central, Alpi in the Siberian, Nakhodka in the Northwestern and Slavyansky in the Urals Federal District. As for DIY, in the Northwestern Federal District, the Iskrasoft and the Santa Haus chains went bankrupt, and some retailers in other districts had to reduce their storecount. However, in general, local DIY retailers managed to withstand the financial crisis.

The level of activity on the part of foreign retailers on the Russian retail market varies and depends on the retail sector, although they are widely represented with regard to groceries and DIY retailing. Nevertheless, still many prominent players successfully operate locally in those segments.

Examples of prominent grocery and DIY retailers oerating locally in Russia, 2010.

The expectations of local retail operators regarding future development after the financial crisis vary considerably depending on the retail sector. Thus, in grocery retailing the financial crisis has stimulated market consolidation. One of the biggest deals in 2010 was the acquisition of the Kopeyka chain by the market leader, X5 Retail Group. In addition, the segment witnessed many other takeovers across the country. On the other hand, in the mobile phones retailing, local players became even more optimistic, and got the opportunity for further geographical expansion, when such giants as Dixis and Tsifrograd went bankrupt. Generally, according to PMR report, the retailers remain optimistic regarding the future development of the market.

More information can be found in the report “Retail in Russia 2011 - Regional Focus - Market Analysis and Development Forecasts for 2011-2013” by PMR.

To order the report or ask for sample pages contact [email protected]

Contacts

MarketPublishers, Ltd.

Tanya Rezler

Tel: +44 208 144 6009

Fax: +44 207 900 3970

[email protected]

www.MarketPublishers.com

Analytics & News