New Opportunities in Conductive Coatings Markets

21 Sep 2011 • by Natalie Aster

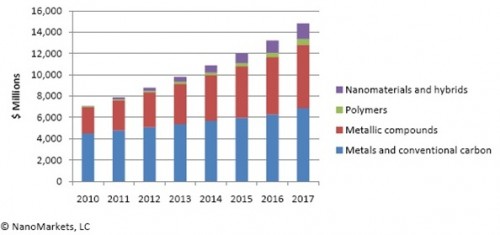

While much of the conductive coatings market involves mature applications and materials, NanoMarkets also believes that there are growing number of newer opportunities for conductive coatings as new types of batteries, displays, lighting and solar panels that are begin to appear on the market. These newer product types will require entirely new conductive materials for their electrodes. NanoMarkets, a leading provider of market research and analysis of the opportunities in advanced materials and emerging energy and electronics markets, estimates that the value of the conductive coatings market will reach $14.8 billion in 2017.

NanoMarkets has been providing analytical coverage of the conductive coatings market for more than three years and has developed an insider’s knowledge of this interesting market. In the report “Conductive Coatings Markets, 2010 and Beyond” NanoMarkets has leveraged this knowledge and identified where the main opportunities in conductive coatings will be found in the next eight years. In particular, NanoMarkets has looked at the new business revenue opportunities for conductive coatings that are emerging from developments in the display, lighting, solar panel, battery and sensor markets.

Conductive Coatings Markets: Materials

Report Details:

Conductive Coatings Markets, 2010 and Beyond

Published: August 2010

Price: US$ 2,995.00

Report Sample Abstract

Not Just Metals Anymore

Traditionally, and for obvious reasons, conductive coatings have been metals. The major exception to this rule is where the coating has had to be transparent as well as conductive, as in the display and thin-film solar panel industry. In such cases, transparent conductive (metal) oxides (TCOs) have been used, with indium tin oxide (ITO) the leading material because of its relative good tradeoff between transparency and conductivity; although the most recently evolved thin-film PV technologies have used aluminum zinc oxide (AZO) and fluorine zinc oxide (FTO).

Much bigger than these trends we believe in terms of generating new business revenues for the conductive coatings industry is the use of nanomaterials and conductive polymers in commercial conductive coatings. Trends in the electronics industry, particularly miniaturization and the ubiquity of wireless communications are also providing opportunities for firms in the bulk conductive coatings space.

Generally, low-cost manufacturing techniques can be employed for producing conductive coatings, including evaporation, solution-processing and thermal transfer. Printing processes, such as inkjet, flexo, and gravure printing are also growing in importance. Sputtering, physical vapor deposition (PVD), chemical vapor deposition (CVD) and atomic layer deposition (ALD) are employed in various applications requiring thin film formation.

More Material Options

The materials used to form conductive coatings fall into four categories: metals, metal oxides, conductive polymers, and nanomaterials. Metallic coatings exhibit the highest conductivity, particularly in nanomaterial form, and according to NanoMarkets’ analysis will account for nearly half of sales in 2017. Metallic oxides, which will make up the second largest category in 2017 based on value, are generally orders of magnitude less conductive than metals, but are often useful because they are transparent. Conductive plastics are also far less conductive than metals and thus will only account for less than 5% of sales in 2017 (3.7%), but offer greater flexibility and lower cost. Nanomaterials, which also include metals and metal oxides, are a newer category and technology, but of growing importance, and will account for nearly 10% of sales in 2017.

Metals: Of the common metals used in conductive coatings, silver is, of course, the most conductive and is widely used for electrodes, but it is relatively expensive and – as we are seeing all too clearly at the present time -- its price can fluctuate with changes in the world financial markets. Coatings tend to use very small amounts of silver. But when the price of silver is as high as it is now, cost can still make a difference.

Still the silver coatings business is protected from substitutions by the fact that alternatives to silver have some pretty serious issues of their own, so the switching costs involved for users who want to move away from silver can be quite significant. Copper and aluminum are the obvious substitutes, but they have handling, performance and corrosion problems that must be coped with. Despite its expense and price fluctuations, gold is used for gold plating of contacts in high-end video equipment and implants for humans and animals (due to its inertness), but gold coatings are never going to be where users of silver coatings are going to be headed when they want to abandon silver. Carbon-based inks are used where maximum conductivity is not a critical requirement.

NanoMarkets expects demand for alloys and other metal derivatives to increase as the prices of common metals used in conductive coatings rise. Combinations such as silver-plated copper or silver and carbon can reduce the cost of thick-film pastes or increase conductivity without reducing transparency. Organometallic compounds have been used in antistatic coatings, printed circuits, EMI shielding and ink jet applications.

Metallic oxides: Although metallic oxides are not as conductive as metals, they still are widely used as conductive coatings, either because of their lower cost or their transparency. The fragility and cost of ITO (which depends on the price of indium), however, are significant limitations of the material and are providing incentive for development of ITO alternatives, although manufacturing improvements still present an opportunity to achieve cost reductions. And, as we have already noted, in certain applications, other TCOs offer superior cost/performance ratios to ITO. We have already mentioned AZO and FTO for use in thin-film PV panels. Indium zinc oxide also has a fragile share of the display market, mainly because of its use at Samsung.

And despite its issues, NanoMarkets expects ITO to continue to dominate the high-end transparent conductor market for a long time to come.

Conductive Polymers: Conductive polymers of interest include derivatives of polyaniline, polypyrrole and polythiophene, as they are commercially available in sufficient quantities, are stable in air and easy to apply. Because they can be transparent and have flexibility, conductive polymers are being evaluated as possible ITO replacements in touch screens and flexible displays. Other potential applications include smart windows, smart fabrics and sensors, which, to return to our remarks at the beginning of this article, are all expected to be growth applications over the next decade. Still, despite their commercial potential, we should note that conductive polymers show relatively low conductivity, and thus they have limited use for high-performance applications.

The most well known conductive polymer - PEDOT: PSS – is doped poly(3,4-ethylenedioxythiophene) (PEDOT). It is offered as a water-based dispersion of submicron-size gel particles of the polymer that form continuous, transparent films upon drying. It has traditionally found its widest use in application in antistatic coatings, but it is encouraging to see it creep into other applications in supercapacitors, OLEDs and as an ITO substitute for displays that do not need very high-performing electrode materials.

Other conducting polymers include polyselenophene (PEDOS), the selenium analog of PEDOT and 3,4-phenylenedioxythiophene (PheDOT).

Nanomaterials: Compared with the other materials used in conductive coatings, nanomaterials are at an earlier stage of technological and commercial development and therefore have the potential to make a leap forward in performance and price.

NanoMarkets believes that it would be hard to overestimate the potential that nanomaterials have for transforming the conductive coatings industry in terms of the performance improvements in the coatings and hence in terms of expanding the addressable markets for these coatings. Coatings, pastes and inks made with nanomaterials can be more conductive due to the increased physical contact between the much smaller particles. Nanocoatings can also potentially be thinner than other kinds of coatings and may dry faster.

The greatest potential impact for nanomaterial-based coatings is perhaps as functional inks and pastes, especially nanosilver inks, in high-end transparent conductive coatings. Nanomaterials may also be used to develop conductive coatings for electrodes in next-generation applications that require higher conductivity, lower processing costs and other performance features that only nanomaterials can provide.

Not surprisingly, nanosilver is the most common nanomaterial being developed, but products with nanocopper and carbon nanotubes (CNTs) are also being produced, and coatings containing graphene or non-carbon nanostructures are at the research stage. Carbon nanotube coatings can be made transparent and are very strong and flexible. NanoMarkets believes they represent one of the best material options for providing an alternative to costly, brittle ITO films. Not only is their long-term potential for low cost attractive, but their flexibility makes them ideal for the growing number of flexible electronics applications.

More information can be found in the report “Conductive Coatings Markets, 2010 and Beyond” by NanoMarkets.

To order the report or ask for sample pages contact [email protected]

Contacts

MarketPublishers, Ltd.

Tanya Rezler

Tel: +44 208 144 6009

Fax: +44 207 900 3970

Analytics & News