Globalisation Drives Green Consulting Sector to $25bn

17 Jun 2011 • by Natalie Aster

- A dozen firms are spearheading the globalisation of the environmental consulting (EC) industry, together accounting for almost a quarter share of the total US$25.4bn global market;

- Their combined EC revenues have increased by 51% during the last four years to reach $6.2 billion in 2009/10 in spite of a market slowdown in the wake of the global financial crisis;

- The global market is set to reach US$30.0bn in the next five years, with a 50% increase in worldwide demand for climate change & energy consulting services.

Increasingly, multinational companies are demanding seamless global service provision from a select list of suppliers, but only a handful of operators in the environmental consulting field are in a position to offer this. In its latest research report “Global Environmental Consulting Strategies and Competitor Analysis 2011”, Environment Analyst provides a unique statistical-based assessment and independent analysis of the regional EC operations, market positioning and business strategies of the largest and most globally-ambitious firms active in this rapidly-evolving marketplace.

Although the global EC sector remains highly fragmented, twelve EC practices have collectively grown their sales by over $2 billion in the last four years to capture a 24.3% slice of the total market worth US$25.4 billion in 2009/10. They are (in order of ranking by global gross EC revenues): URS Corporation, CH2M Hill, Arcadis, Golder Associates, Environmental Resources Management (ERM), MWH Global, RPS Group, AECOM, Parsons Brinckerhoff (Balfour Beatty), Environ, WSP Environment & Energy and WorleyParsons.

NYSE-listed engineering and construction services group URS leads the pack, and is the only player with a global EC market share in excess of 5% – largely thanks to its strong position in the dominant North American sector. URS significantly expanded the international reach of its EC business – particularly in the European, Middle East/Africa and Asia-Pacific regions – with its acquisition of Scott Wilson in September 2010. According to the report, URS is the market leader in no less than four out of the six major EC service disciplines – including the largest, contaminated land. URS also benefits from a strong public sector client base, deriving 45% of its total EC revenues from governments & regulatory bodies/agencies.

Report Details:

Global Environmental Consulting Strategies and Competitor Analysis 2011

Published: June 2011

Pages: 115

Price: US$ 1,965

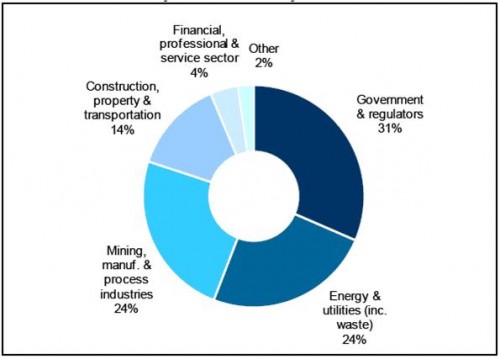

Based on aggregated financial data for the “Global 12” firms, contaminated land related services are estimated to account for 41% of their combined annual EC revenues in the last financial year. Extrapolated to the global market as a whole, this is equivalent to a total market sector worth US$10.5 billion. Contaminated land is followed by water & waste management (22%) and environmental impact assessment (EIA) & sustainable development (14%). Looking at a breakdown by major client sector, the largest single spend comes from government & regulators at $8.0 billion – or 32% of the total – followed by utilities & energy firms (24%).

The Global 12’s combined EC revenues declined by 1% in 2009/10 – reflecting market deterioration in the wake of the global financial crisis. There are signs that demand in key areas of the private sector are increasing again, although the public sector will remain constrained for the medium term, particularly in Western Europe. Taking into account regional and sectoral variations, the global EC market is projected to reach US$30.0 billion by 2014/15 – equivalent to an 18% increase and an additional US$4.6 billion in revenues in the next five years.

Liz Trew, Editor of the Environment Analyst Market Intelligence Service, comments: “Growth will be much more sector-specific than in the environmental consulting boom years prior to the global economic downturn, with climate change and energy services driving market recovery thanks to the strong underlying legislative and political drivers. Growth in this sub-sector is expected to be around 50% over the next five years.

“Regionally, economies that are led by natural resource industries rather than manufacturing or services will be more buoyant. This is reflected in the significant levels of investment we have seen recently from the Global 12 in countries such as Australia, Brazil, Canada and South Africa.”

Global environmental consultancy market share by client sector 2009/10

More information can be found in the report “Global Environmental Consulting Strategies and Competitor Analysis 2011” by Environment Analyst Publishing & Research.

To order the report or ask for sample pages contact [email protected]

Contacts

MarketPublishers, Ltd.

Tanya Rezler

Tel: +44 208 144 6009

Fax: +44 207 900 3970

Analytics & News